Is There a Foreclosure In Your Future??

You May Have A Better Way Out!

There are many instances where your mortgage may become unaffordable. It may be a loss of a job, medical bills or even a hike in mortgage payments. But ignoring the bills will not make them go away, it will only make things worse.

If you need help, there are approaches that can help, but you may not be familiar with them. One of these is a “short sale.”

A short sale is a sale of real estate in which the proceeds from the sale fall short of the balance owned on a loan. In a short sale, the bank of the mortgage lender agrees to discount a loan balance due to an economic or financial hardship on the part of the mortgagor. This negotiation is done through communication with the bank's loss mitigation department.The homeowner will sell the mortgaged property for less than the outstanding balance of the loan and then turns over the proceeds of the sale to the lender, usually but not always fully satisfying the debt.

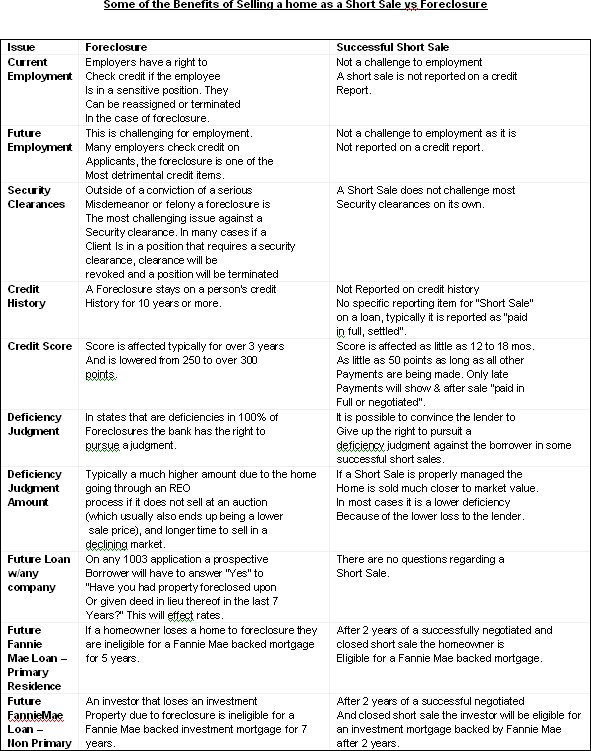

A short sale typically is executed to prevent a home from forclosure. For the homeowner some of the advantages are avoidance of forclosure on their credit history, partial control of monetary deficiency and is typically faster and less expensive than a forclosure.

In an approved short sale, the lender agrees to accept less than is owed for the property, and the homeowner is relieved of the debt. A lender may be willing to do this because it spares a lot of hassle and expense involved in executing a foreclosure. And typically, a short sale does far less damage to the homeowner’s credit than a foreclosure does.

If you would like to explore the possibility of a short sale for your property, avoid foreclosure, and potentially save your credit rating, contact The Stephan Moret Team.